![[XDT]CREATE MORE Act (RA 12066) THUMBNAIL](https://www.xdtgroup.ph/wp-content/uploads/2026/03/xdtcreate-more-act-ra-12066-_thumbnail.png)

By: John Joseph Cedo – Business Unit 3

The Philippines has enacted considerable tax reforms in recent years to reform the tax system, attract investments, assist small enterprises, and stimulate economic growth. The Corporate Recovery and Tax Benefits for Enterprises (CREATE) Act, passed in 2021, made a substantial impact by lowering corporate income tax rates and updating tax benefits. Following this, the President of the Philippines signed the CREATE MORE (Maximize Opportunities for Reinvigorating the Economy) Act on November 11, 2024, to improve and broaden incentives to help boost economic recovery, support businesses, and attract foreign investment. We examine the CREATE MORE Act’s key components and potential benefits here.

Corporate Income Tax Rate for Registered Business Enterprises

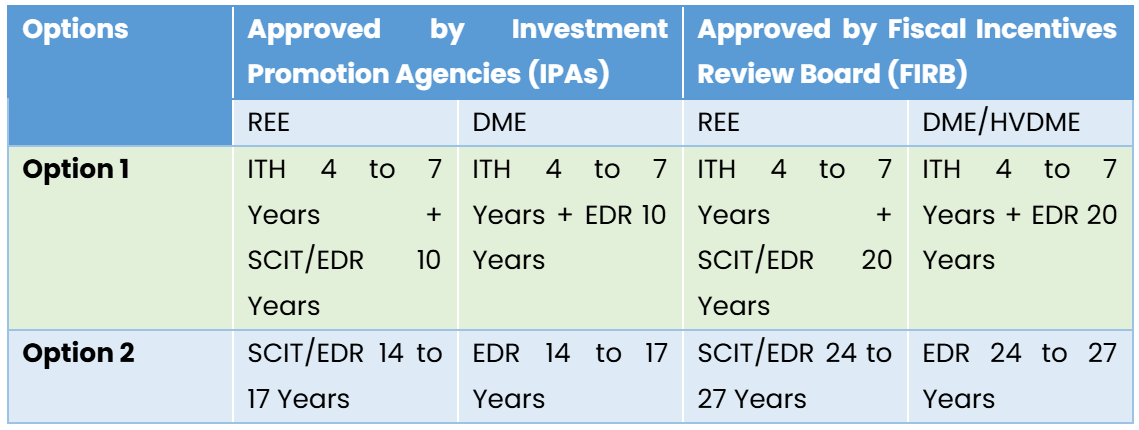

One of the most significant changes is the implementation of the 20% Corporate Income Tax (CIT) Rate for Registered Business Enterprises (RBEs) under the Enhanced Deductions Regime (EDR) on taxable income received from registered projects or activities during the taxable year.

The earlier EDR under the CREATE Act permitted firms to make additional deductions. Under the CREATE MORE Act, the 20% tax rate effectively reduces firms’ overall tax liability and allows them to claim EDR on qualified expenses.

This shift answers the Organization for Economic Co-operation and Development’s (OECD) Pillar Two Global Minimum Tax (GMT) rate requirement of 15%. By instituting a 20% tax rate under the EDR, the Philippines establishes a clear tax framework that allows enterprises to comply with global standards while maintaining large deductions for R&D, training, and other qualified expenses.

Expanded deductions under the Enhanced Deductions Regime

Another notable change is the increased percentage of deductible spending items under the EDR, which would further incentivize firms. For example, the Act raised the extra deduction for power expenses from 50% to 100%, making it more appealing for businesses to engage in energy-intensive areas like manufacturing and logistics.

The Act also includes new deductible expense items for trade fairs and exhibitions, which can help firms expand their market reach and promote their products locally and worldwide. The Act now allows Net Operating Loss to be carried forward as a deduction for the next five (5) consecutive taxable years immediately following the last year of the project’s Income Tax Holiday (ITH) period rather than the year of such loss.

Eligibility conditions for registered business enterprises

Under the CREATE Act, incentives were exclusively accessible to registered export businesses (REEs) and domestic market enterprises (DMEs). The CREATE MORE Act eases this criterion by broadening the definition of qualifying businesses to include “registered business enterprises,” which now include international and domestic businesses under specific conditions. This amendment will widen the list of enterprises eligible for EDR and SCIT options to promote the Philippines as an appealing investment destination for domestic and foreign investors.

VAT Exemption and Zero-Rating

1. Eligibility Criteria for VAT Exemption and Zero-Rating

VAT incentives will apply to items and services “directly attributable” to a registered company’s initiative or operation. This explains the rules for VAT incentives outlined in the CREATE Act, which were previously ambiguous and subject to multiple interpretations, causing challenges with implementation.

The CREATE MORE Act states that the following items and services if utilized directly in the registered activity, will be eligible for VAT exemptions or zero-rating:

- Janitorial Services

- Security services

- Financial Services

- Consulting services

- Marketing and Promotional Services

- Administrative activities include human resources, legal, and accounting functions.

2. Conditions for VAT Exemption and Zero-Rating

Further, the CREATE MORE Act specifies the conditions under which VAT exemption and zero-rating apply.

- VAT Exempt: Importation of goods by an REE whose export sales are at least 70% of the total annual production of the preceding taxable year;

- 0% VAT: Sale of goods and services to/for REE whose export sales are at least 70% of the total annual production of the preceding taxable year or

- 0% VAT: Sales to bonded manufacturing warehouses of REE

This clarification ensures that companies understand which services are eligible for VAT relief, preventing abuse of the incentive and ensuring that only activities directly related to the core operations of a business benefit from VAT exemptions or zero-rating.

3. VAT treatment on the sale, transfer, or disposal of formerly VAT-exempt imported goods

The CREATE MORE Act explains VAT treatment for the sale, transfer, or disposal of previously VAT-exempt imported capital equipment, raw materials, spare parts, and accessories, subject to the following conditions:

- 0% VAT: The buyer is a REE (independent of location);

- 0% VAT: The seller is a DME, and the buyer is a REE (regardless of location);

- 12% VAT: If the seller is a DME (regardless of location), VAT will be calculated based on the net book value of capital items or materials.

4. Special provisions for high-value domestic market enterprises (HVDME)

Under the CREATE MORE Act, DMEs with at least PHP 15 billion in investment capital and either import-substitute or cater to non-resident markets, or those with export sales of at least USD 100 million, will benefit from increased 0% VAT on local purchases and VAT exemption on importation.

This clause may encourage significant investment in sectors vital to economic development, such as infrastructure, heavy industries, and export-oriented manufacturing.

Registered Business Enterprises’ Local Tax

Companies that qualify for tax breaks, such as income tax holidays (ITH) or EDR, will be subject to a municipal tax of up to 2% of gross income in place of all other local taxes and fees. This will significantly lessen businesses’ administrative and financial load, allowing them to focus more on their activities rather than dealing with several local taxes of variable complexity.

This would apply during the ITH or EDR period if the RBE is registered with the appropriate IPA and maintains such registration for the ITH or EDR term, as well as meeting the conditions established, such as engaging in export activities or providing critical domestic market services.

As firms take advantage of these tax breaks, the Philippines is expected to see an increase in foreign investment, job creation in high-value-added industries, and the sustained expansion of critical sectors. Hopefully, the CREATE MORE Act will help the Philippines become a strong competitor in the global marketplace, making it an ideal site for businesses wishing to invest, expand, and succeed.

Reference/s:

The CREATE MORE Act (RA 12066): A new chapter for tax incentives and economic development in the Philippines. (2024, November 11). Grant Thornton Philippines. https://www.grantthornton.com.ph/insights/articles-and-updates1/lets-talk-tax/the-create-more-act-ra-12066-a-new-chapter-for-tax-incentives-and-economic-development-in-the-philippines/

![[XDT] RTU Students Take The Next Step Successful OJT Completion At XDT & Company, Inc. Thumbnail (2)](https://www.xdtgroup.ph/wp-content/uploads/2026/07/xdt-rtu-students-take-the-next-step-successful-ojt-completion-at-xdt-company-inc._thumbnail-2-300x300.jpg)

![[XDT] RTU Students Take The Next Step Successful OJT Completion At XDT & Company, Inc. Thumbnail (4)](https://www.xdtgroup.ph/wp-content/uploads/2026/07/xdt-rtu-students-take-the-next-step-successful-ojt-completion-at-xdt-company-inc._thumbnail-4-300x300.png)

![[XDT] RTU Students Take The Next Step Successful OJT Completion At XDT & Company, Inc. Thumbnail (1)](https://www.xdtgroup.ph/wp-content/uploads/2026/06/xdt-rtu-students-take-the-next-step-successful-ojt-completion-at-xdt-company-inc._thumbnail-1-1-300x300.png)

![[XDT] RTU Students Take The Next Step Successful OJT Completion At XDT & Company, Inc. Thumbnail (1)](https://www.xdtgroup.ph/wp-content/uploads/2026/06/xdt-rtu-students-take-the-next-step-successful-ojt-completion-at-xdt-company-inc._thumbnail-1-300x300.png)